- There were clear winners & losers in the 1st quarter of 2017.

- Your performance depends on where you placed your bets.

- If you bet on Trump making the stock market great again, you were a winner.

- If you bet that foreign stock markets would outperform the U.S., you were a winner.

- If you bet that energy stocks would rebound, well… maybe next time.

The first three months is in the record books, and there are some clear Winners & Losers In The 1st Quarter Of 2017. If the real estate game is all about location, the investing game is all about asset allocation. Security selection is also a critically important part of success, but even the best traders will have a tough time capturing alpha at the portfolio level if they’re overweight an asset class that’s out-of-favor.

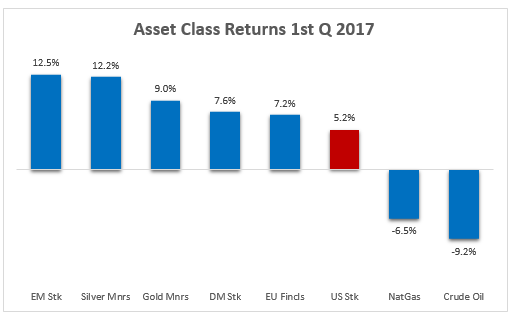

To illustrate my point, let’s look at the performance of various asset classes over the course of the first quarter. In the chart below, I selected the asset classes that had the largest moves either up or down. Since most of my readers are U.S. based, I’m going to use the U.S. stock market as my point of reference for comparison.

It should be apparent from the chart that there was a wide variation in the returns of these asset classes, and this supports my view that asset allocation is a critical component of portfolio returns.

Let’s say that you’re one of the millions of investors who favor U.S. stocks over non-U.S. stocks. In the 1st quarter, this home-country bias would have cost you in terms of portfolio alpha. Both Emerging Market stocks and Developed Market stocks outperformed their U.S. cousins by a wide margin.

Gold and Silver Miners outperformed U.S. stocks as well. Even the wildly unpopular European Financials did better than their U.S. rivals. Let’s look at the Winners & Losers In The 1st Quarter Of 2017.

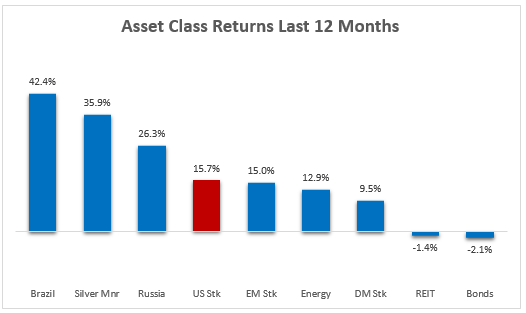

Next let’s look at the asset class winners & losers over the last 12 months. The variation in returns among the classes is much wider, which further underscores the importance of diversification. The $64,000 question is how to diversify effectively.

There are many ways to approach the diversification issue, and nobody can claim that their strategy is the ultimate solution. But the approach that has worked the best for me and my clients over the years is a rules-based, mean-reversion strategy.

I won’t go into details here, but I’ll give you an overview. I start with a generic allocation across the major asset classes, with each allocation based on the relative weight of the asset class in the global capital market portfolio. This is the starting point, or the baseline.

Next I adjust each allocation based on current valuations relative to long-term average valuations. You can do this with several metrics, such as the distance from the 200 day moving average, the median P/E or P/B or (in the case of bonds) the spread over the riskless rate.

Precious metals, and the miners who extract and sell them, have their own valuation metrics, as do commodities like oil and natural gas. But the goal is to look for extremes in valuation based on metrics that are relevant to the specific asset under consideration.

Mean reversion is a bedrock principle of the capital markets. Whatever methodology you use to identify extreme valuations, the basic idea is the same. Periodically rebalance your allocations, adding to undervalued assets and trimming back on overvalued ones.

There’s no magic formula, just a healthy dose of common sense. And the most important part of the process is consistency and discipline.

Once you figure out your valuation metrics, convert them into specific trading/rebalancing rules that you can follow faithfully. If they aren’t producing the results you expect, then tweak them. But don’t make the mistake of changing strategies every time you have a bad month or quarter. It takes time for a strategy to play out in real time, so lots of patience is required.