The case for continuation of the bull market

One of the key skills shared by all great traders and investors is the ability to imagine a set of possible outcomes that could result from a trade under consideration, and then assign a probability to each of the outcomes. It’s more of an art than a science, because after all, we’re talking about the future. My preferred method for doing this calculaltion comes from the work of Thomas Bayes, who developed a methodology whereby he began with an educated guess about possible outcomes, and then he refined those guesses, based on the historical record of what has happened in the past under similar circumstances. It’s a very effective way to improve the accuracy of your initial estimates.

The question I will consider today is, “How likely is it that this bull market is over?” Using Bayes’ methodology, the first step is to clearly define our terms, and what parameters we will use for the calculations. Here are the terms and conditions I have chosen for this task:

The bull market is over.

If the S&P 500 declines by 20% from its most recent high-water mark of 2872, before it makes a new, higher-high, the bull market is over.

The bull market remains in force.

This is simply the inverse of the above. The market makes a new high before it declines by 20% from the recent high.

These two outcomes are mutually exclusive, and they represent 100% of the possible answers to the original question. In other words, there is no third possible outcome. It’s a binary choice – yes or no, up or down, dead bull or living bull.

Before I get into the details of the Bayes methodology, I’d like to take a moment to tell the story of three friends who went to Las Vegas to gamble and have some fun. Each of them has their own unique approach to gambling, and how likely it is that they will come home as a winner or a loser. The answer depends on how skilled they are at calculating probabilities for each individual bet they make, and how much attention they pay to money management.

These skills are similar to those used by stock market investors, with one exception. In Las Vegas, the task of calculating the odds of any particular bet paying off is more simple and straightforward than our bear market question. You’ll see what I mean as we work through the process.

The odds

Every game in the casino has a specific set of odds. The casino will not operate a game that has negative odds for them, so it’s just a matter of how fat they can make the odds on each game while still attracting action.

For example, Blackjack has the best odds of winning, with a house edge of just 1 percent in most casinos. Plus, you are playing against the dealer, not professional card sharps. Players who can count cards will actually tip the odds in their favor, which is why casinos ban them from playing if they suspect they are counting cards.

Craps is the game with the second-best odds, also nearly 50-50. The craps table can be a bit intimidating for the beginner with all the betting choices, but it’s really not tough, and it has one of your best chances of winning. In the end, all you are really doing is betting on a roll of the dice.

Wheel of Fortune and slot machines have the lowest odds of winning, with a house edge of 10 percent or more. There are many other games in the casino, like Keno, that are suckers’ games. But people play them because they’re fun!

The most attractive odds for players in any casino is poker – hands down. Why? Because poker is primarily a game of skill, with an element of luck in the short-term. Annie spent most of her time playing poker, and she left Vegas $10,000 richer.

The best investors understand the odds

Let’s look at the odds of various outcomes for the market, based on Bayes Theory of Probability.

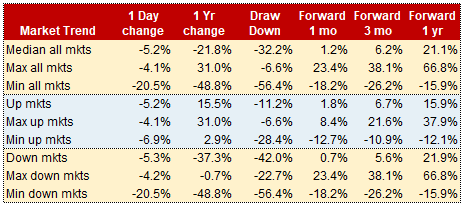

Table 1 shows the history of the 42 worst 1-day drops in the S&P 500 since 1950. There’s a lot going on in this table, but don’t worry – I will drill down on each section and explain what everything means as we go along.

After gathering a list of the worst 1-day drops in the market, I organized this table into three parts. 1. All markets, whether bull or bear or sideways. 2. Up markets, because there is a different dynamic at work when the big down day comes after the market has been going up. 3. Down markets, for the same reason. The dynamics at work are different when the big down day comes after a losing year in the market.

Table 1

A quick glance at table 1 provides some clues about what happens after a big 1-day drop in the market. It shows the 1-day drop, the 1-year performance leading up to the big drop, the drawdown, which is the total decline from the previous high-water mark, and the performance of the market over the next 1, 3, and 12 months. I will drill down into each of the three categories in a moment. The categories are all markets, up markets, and down markets. We can pick up clues from each of these categories.

Key observations from Table 1: The good news is that the most likely outcome 1 year after a very big one-day drop like we saw on February 5, is a gain of 21.1%. The range of 1-year outcomes is wide, from up 66.8% to down -15.9%. What this tells us is that after a big down day in the market, there has never been a bear market one year later. That’s significant.

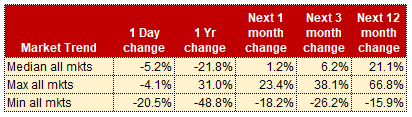

Table 2

In this table, I included all the returns that were recorded after each of the 42 biggest one-day market drops. This table looks at the big picture – how has the market performed after these big declines, regardless of what took place in the year leading up to the decline.

Note that the “base case” which includes all 42 of these big 1-day drops, indicates that the most likely outcome over the next 12 months would be a gain of 21.1% from Monday’s closing price. There is a wide range of recorded outcomes.

The best outcome came after the last gasp of the 2009 financial meltdown took place, and the market gained 66.8% over the next 12 months. The worst outcome came in September, 2001. After the Twin Towers came down, the country and the market struggled to regain their footing.

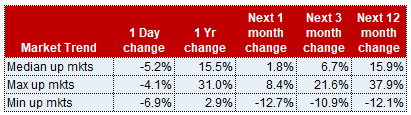

Table 3

Next is the performance of the market after a big decline that was preceded by a strong market. The average return 1-year later is a gain of 15.9%. Again, this is good news for us.

This table is the most relevant to our current market environment. We have just come from a very strong period in the market, so it’s informative to take note of what has happened in the past after a big drop.

When we look at all of the big down days that have been preceded by a healthy market, we see that the average gain over the following 12 months is 15.9%. This is encouraging news for us today. But it’s far from a guarantee.

The best outcome on record was August, 1998. This was in the middle of the great bull market of 1982-2000. In late 1998, the Asian crisis hit, and there was widespread panic that the entire financial system might collapse. Once the problem was resolved, the market took off again.

The worst outcome was in April, 2000. The tech bubble had burst, and investors were fleeing the market in droves. One year later, the market was down by 12.1%, and there was much more pain to come.

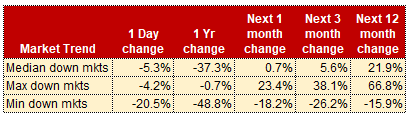

Table 4

Finally, the performance of the market after a big decline that was preceded by a weak market, is better than those preceded by a strong market. The average gain after weak markets is 21.9% one year later. Once again, this is good news, but our category is an up market. This means that our expected return one year from now is 15.9%, compared to an expected return of 21.9% after a weak market. Still good news, but not quite as good as it could be.This table focuses exclusively on big 1-day drops that were preceded by a weak market over the prior 12 months. As you can see, the outcomes going forward are very different, and much more positive, for this group.

While the up market events produce an average gain of 15.9%, the down market events are followed by gains of 21.9% on average. The range of outcomes is wider, and better, too. The best 12 month return after an up market was 37.9%, compared to 66.8% after a down market.

This isn’t hard to understand, if you’re a contrarian like me. Reversion to the mean is a powerful force in the market, as these tables show.

We’re on the wrong side of history today

The correction we’re in now is coming after a roaring bull market. That puts us on the wrong side of history, because bull market corrections don’t tend to do as well as bear market corrections. It’s not a death penalty for our current bull, but it does make the odds of making a new high a little thinner.

What can we learn about the odds of possible future outcomes?

You can, and should, come to your own conclusions about what this data means. I hold no claim to the perfect truth in this, or any other matter. But I do know a few things about probability and odds. Here’s my personal opinion, based on the work of Thomas Bayes:

- The most likely outcome, at 62% odds, is that the market will make a new high before it completely rolls over into a new bear market.

- The next most likely outcome, at 22% odds, calls for a deeper and longer correction that stops short of a new bear market.

- The least likely outcome, at 16% odds, is that the market fails to take out the old high-water mark, then rolls over into a bear market that could even lead to an economic recession.

These probabilities are cause for concern, but not for radical changes to your portfolio.

My factor-based trading strategies have been holding up nicely during this stressful time in the market. Be sure to check out my Trading Strategy page here.