Happy Days Are Here Again – 1930’s Version

In the depths of the great depression of the 1930’s, President Franklin Delano Roosevelt rallied the people by offered an uplifting message of hope that there were better days ahead. This sentiment was captured by the song “Happy Days Are Here Again” which played everywhere, and continuously. And it worked… for a while anyway.

By itself, the song couldn’t make the bread lines go away. It couldn’t put people back to work. And it certainly couldn’t make the economy pull out of the Great Depression. But what the song could do, and did do, was give people hope that the government was coming to the rescue, and soon we would return to an era of growth and prosperity.

Today the U.S. is in far better shape than we were in the 1930’s. Depending largely on how you view the current political and economic landscape, you either believe or don’t believe that happy days are here again. For some, it’s blue skies and roses. For others, there’s danger all around. Let’s dive into the details and try to come up with a reasonable assessment of where we are as a nation.

Happy Days Are Here Again – 2018 Version

We are now within 3% of the all-time high for the S&P 500. What’s an investor to do?

To begin with, we need to remove all political biases from the discussion. This is not going to be a partisan rant about what’s wrong in Washington. It’s going to be a non-partisan assessment of what’s happening to the economy, the stock market, and the future of America.

Let’s assume, for argument’s sake, that I’m a staunch Republican and an enthusiastic backer of Donald Trump and his policies. I believe that President Trump will bring back high-paying factory jobs, rescue the coal industry, build his great wall on the Southern border, renegotiate our bad trade deals in our favor, and work tirelessly for the interests of the little guy – the forgotten middle class worker who has been shafted repeatedly by the system. It’s an ambitious agenda, but I believe that Trump will fulfill his campaign promises.

I don’t believe that Happy Days are Here Again

As I said, I’m a Trump supporter because he’s the president we have. When Obama was president I was an Obama supporter. Same with both Bushes and Clinton. The only president I did not support was Nixon. My mom once told me that Nixon was so crooked that his aids had to screw him into his pants every morning.

It makes no sense to me for an investor to make decisions based on their political point of view. Investment decisions should be based on the reality of what’s happening in the economy and the stock market. The stock market doesn’t care about which party is in control in Washington. It only cares about economic growth and earnings growth. Period.

Trump has convinced roughly half the country that happy days are here again. But the other half, including me, remain skeptical. It’s in my job description to always be skeptical until I can gather enough hard evidence to support a point of view. So my attitude, to quote Trump himself, is “Let’s see what happens.”

What we know, and what we don’t know

Here’s what I know. There are always two sides to the story when it comes to our future prospects. There’s an optimistic story and a pessimistic story. But there is also a third story that isn’t colored by the bias of optimism or pessimism. It’s the evidence-based story, and it has no political element, no optimism or pessimism bias, and no reliance on songs or slogans that are meant to drum up support for the party who happens to be in charge at the moment. I will discuss all three stories.

The Optimistic Story

The optimistic story is based on several memes that are repeated by the party in power. For example:

- The global economy is booming,

- Unemployment is historically low,

- Interest rates are still low,

- Corporate earnings in the U.S. are strong and growing,

- The threat of a nuclear confrontation between North Korea and the U.S. have been eliminated,

- It’s only a matter of time before high-paying factory jobs will return to America from overseas,

- The coal industry is coming back strong, putting miners back to work,

- The Great Wall on our Southern border will get built eventually,

- Congress will approve a massive new spending bill to rebuild our crumbling infrastructure,

- The massive tax cuts for corporations will lead to a surge in capital expenditures and millions of new jobs,

- We will renegotiate all of our trade deals, or just pull out of them, and that will boost our exports and eliminate our trade deficits.

- The generous tax cuts to the most wealthy citizens will trickle down to the rest of society as they buy more refrigerators, dishwashers, cars, yachts, and fine art.

The Pessimistic Story

On the negative side of the ledger are:

- The U.S. national debt and budget deficits have ballooned to the point where some economists are sounding the alarm.

- Geopolitical risks are elevated, regardless of the peace overtures with North Korea, a notorious reneger on past deals.

- Iran and the Middle East. Now that we have pulled out of the nuclear deal, Iran is free to pursue their program with vigor and speed. That can’t be good for peace in the Middle East.

- Russia, under the reign of Putin, is hell-bent on dominating Europe and gaining a seat at the table for all future negotiations about the direction of NATO. President Trump has publicly lobbied to re-admit Russia to the G7.

- Russia is also determined to destabilize American Democracy, by interfering with our elections and using sophisticated hacking and social media programs to encourage distrust of the government, and further polarize our citizens.

- The move towards deregulation, especially for the banks, is greasing the skids for another financial meltdown.

- The Fed is now in tightening mode. Higher rates, less liquidity, fewer bail-outs.

- Corporate earnings are benefiting from the recent corporate tax cuts. Once this stimulus wears off, earnings will return to normal, and stock market valuations will come down.

The Evidence-Based Story

When we strip out the political bias, the hyperbole, and the unsubstantiated claims, we are left with these points.

- The U.S. stock market is expensive, based on several measures. Cyclically Adjusted P/E, Percent above trend, Percent of Gross Value Added, Percent of GDP, Price-to-Book, and others. The only justification for current prices is the hope that corporate earnings will continue on the growth trajectory they have enjoyed for the last 4 quarters. Analysts agree that this is unrealistic.

- We are now 9 years into this bull market and economic expansion. While there is nothing to suggest that these trends are close to the end of their run, a rational investor must take into account that economic and stock market history, along with the immutable laws of mean-reversion, will re-appear.

- There are pockets of extreme over-valuation in today’s marketplace. Cryptocurrencies, Tech Unicorns, and Venture Capital to name just three. Every bear market begins with a bubble popping somewhere.

- The hottest business model today is the MoviePass model. Offer a deep discount to a specific consumer favorite, take a loss on each transaction or membership, and hope to make it up on volume. Does this make sense to you? The way these businesses stay afloat is by attracting outside financing from Venture Capitalists. The new money coming in the door pays for the losses going out the door. Eventually, gravity takes over and the business fails, or it gets bought by Google.

- In spite of what you may have heard from your local politician, debt matters. A lot. Recall that the Republican party once stood for fiscal responsibility. No more. Now they say that debt doesn’t matter. I understand why they have changed their tune. They have now presided over the largest expansion of our national debt since WWII. And interest rates are on the rise, which means it is becoming more expensive to service the national debt. Debt has consequences.

- Tariffs. The U.S. has tried, over and over again, to impose trade tariffs on countries who were selling more goods to us than we were to them. As Trump says repeatedly, “very unfair.” Problem is that tariffs don’t work. Never have, never will. Just look at history. The first time we tried it was the Tariff act of 1789. It succeeded in one sense – it brought in revenue to the U.S. Treasury. There was no income tax at the time. But it hurt trade then, as it will now. If you raise your tariffs, we will retaliate, as Justin Trudeau recently remarked at the G7 conference.

- Homeland Security: The enormous cost of defending against Muslim terrorism. It is far less likely that an American citizen will be killed in a terror attack than just about anything else. According to Nicholas Kristof of the New York Times, “Most years in the U.S., ladders kill far more Americans than Muslim terrorists do. Same with bathtubs. Ditto for stairs. And lightning.” Why does the U.S. spend billions every year on anti-terrorism measures? Because they make for scary headlines. Domestic terrorists are responsible for 25 times as many American deaths than Muslim or foreign terrorists.

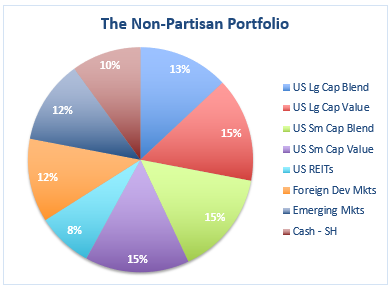

The non-partisan, apolitical portfolio

How can we boil all of this down into a political and ideological bias-free portfolio? Here’s my offering.

The nature of this portfolio is to be 100% invested in global equities at all times, except during serious market declines. Declines are telegraphed by a Bayesian Probability Model that takes into consideration valuation, market internals, where we are in the business cycle, and coincident indicators like industrial production.

Here is the asset allocation of the portfolio.

And here are the stats of the performance from 1972 to 2017.

| Initial Balance | Final Balance | CAGR | Stdev | Best Year | Worst Year | Max. Drawdown | Sharpe Ratio | Sortino Ratio | US Mkt Correlation | |

| Portfolio 4 | $10,000 | $ 2,446,256 | 12.7% | 15.5% | 32.2% | -7.8% | -11.9% | 0.56 | 0.73 | 0.94 |

The in-sample (backtested) period was from 1972 to 2003. The out-of-sample period (real time) was from 2004-2017.

Why does this portfolio perform so well?

It all comes down to playing defense. Notice that there is a 10% allocation to “Cash – SH.” The cash allocation offers two advantages. It stands at the ready to take advantage of market declines that are not associated with recessions, and therefore are shorter in duration and more shallow. The SH allocation provides the option of going short the S&P 500 index when appropriate. One could use other short vehicles, but for purposes of this article I use SH.

How does one know when to go short?

Each investor must develop his or her own way to make this determination. For me and my clients, I use a Bayesian Probability Model. When my model reaches 50% likelihood of a bear market within the next 12 months, I initiate defensive steps to protect the portfolio. At first, I reduce exposure to the most volatile holdings. Next, I reduce exposure to the largest holdings. And if the signal persists, I begin to initiate a short position via the short S&P 500 ETF SH.

The added layer of defense enhances overall performance by 200-500 basis points per year over the life of the portfolio. This contributes enormously to final wealth at retirement.

As always, comments and questions are welcomed.