“Come, Watson, come. The game is afoot! Not a word!”

From The Return of Sherlock Holmes by Arthur Conan Doyle

The ZenInvestor Intelligence Report is a monthly publication for subscribers who want two things: To stay ahead of the next bear market, and to get early warning of the next recession. This article is from June 2018 and is intended to give readers a sense of our thinking on these two important points.

Highlights

• This month we get our first recession warning since 2007.

• Key Market Indicators slipped a bit more during May.

• Remember that the market is only 4% below it’s high-water mark.

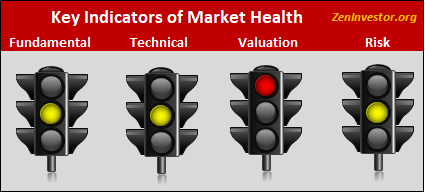

Key Market Indicators (KMI)

The KMI model, shown at the right as traffic lights, slipped last month. We still don’t have an outright sell signal, but conditions are rather fragile right now. There is an abundance of uncertainty hanging over the market like a storm cloud. Geopolitical, policy, trade, interest rates, budget deficits, and the list goes on.

The stock market does not do well in times of heightened uncertainty, and today is no exception. Let’s go through the indicators to get a sense of the health of the market.

Fundamentals. After serving as a dependable anchor for many months, the fundamentals that underpin the market are now flashing Yellow. The proximate cause was a squeeze in profit margins as employment costs continue to rise and interest on corporate debt continues to increase.

Technicals. Yellow light, no change from last month. But the momentum piece of this group of indicators has been deteriorating lately. For the past few years we could count on the dip-buyers to step in and support any weakness in the market. But now they are being challenged by the new kids in town – the rally-sellers. It’s too early to tell which camp will prevail, but the action was enough to flip the momentum indicator from yellow to red.

Valuations. Red light. Valuations have come down somewhat from recent levels, due to rising earnings and falling stock prices, but they are still well above the long-term trend line.

Risk. Yellow light. Recession threat is low, but ticking higher. Bear market threat is moderate but creeping up, and volatility is increasing. Volatility ticked lower this month, but it has returned to the markets, and is unlikely to go away anytime soon. Geopolitical risks are high, and the likelihood of a policy mistake by the Trump administration or the Fed continues to increase.

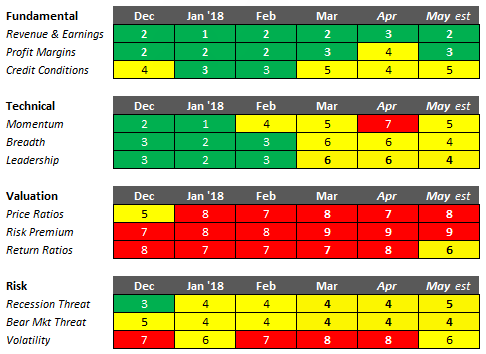

The Data Driving the KMI Traffic Lights

Fundamentals are still supportive, but they are no longer the bulwark that has been supporting this bull market. Revenues, earnings, and profit margins are very strong, but credit conditions are starting to pinch just a bit, due to the increases we’re seeing in interest rates.

Technical underpinnings actually improved a notch from last month, but not enough to flip this indicator from Yellow to Green.

Valuation continues to be the biggest threat to the market. High valuations alone can’t trigger a bear market. They need help from the other indicators, especially Fundamentals. We haven’t reached that point of confirmation yet, and we may not reach a sell signal for several more months or even longer.

Risk is still flashing Yellow, but it actually improved a bit from last month. As long as the threat of recession remains low, as it is today, the correction we’re in should be limited in depth. Duration is another matter, however. We have now spent 78 days under water (below the last high-water mark).

Bear Market Probability Gauge

This is a tool that my clients and subscribers can use to help them make critical asset allocation decisions. This is not a market-timing tool. It’s a dynamic reading of the probability that a new bear market will arrive sometime in the next 12 months. Investors can decide for themselves how to use it. Contact me through the website if you want help setting up your defensive strategy.

As of today, May 31, 2018, the probability of a new bear market arriving within the next 12 months is 24%. That is up from 21% last month, primarily due to the correction and the slowly deteriorating technical readings. Let me stress again, we do not have a sell signal yet. One of my cardinal rules is “Don’t get ahead of your indicators.”

Probability of various outcomes over the next 12 months

Continuation of the bull market 53%

A stock market “melt-up” 3%

Correction of 10-15%, with full recovery 20%

Decline of 20% or more, with no recovery 24%

U.S. Markets

This market is in a funk. Investors can’t decide whether to buy the dips or sell the rallies. It has now been 78 days since the last new high, and that’s fairly significant. Most garden-variety corrections get resolved in 26 trading days, or about 2 calendar months. The longer this correction drags on, the more likely it becomes that it will be resolved by breaking support, which stands at 2,581.

If that happens, investors who pay attention to technical indicators will likely ratchet up their selling. The dip-buyers will be under pressure to step up and provide support in a falling market. At some point, the rally-sellers will overwhelm the dip-buyers. We don’t know when this will happen, but it is a certainty that it will happen eventually.

Are robust earnings growth enough to sustain this aging bull?

Those who remain steadfastly bullish base much of their argument on the robust growth in revenues and earnings. They have a point. Earnings are one of the three main drivers of equity returns, and they deserve careful consideration in the calculus of what’s ahead for stock prices. But earnings are only one of three pillars of stock market returns, the other two being dividend yields and P/E ratios. (See my article about the big three drivers here.)

Robust earnings like we’ve been seeing for the last few quarters are certainly a positive for stock prices, but here’s the thing. The stock market is, among other things, a discounting mechanism. One of the indicators it discounts is earnings growth. I can make a case that the robust earnings we are seeing today, as well as the earnings estimates going forward, have already been priced in to the market. Everybody knows that earnings are strong, and analysts are raising estimates for the next three quarters. This raises an important question.

What will happen when the adrenaline rush from the big corporate tax cuts wears off? My view is that earnings growth will still be strong, but the rate of increase will start to fade. This is just my opinion, but it’s based on what I’ve observed since I started in the business in the 1970’s.

The Market Dashboard

Observations

Drawdowns have now gone through a successful retest of the February low. Whether the market can stay above that level is anyone’s guess.

Net Up days out of the last 21, a measure of momentum, was running above average all throughout 2017. The current reading is two, which indicates slightly upward momentum. When we see readings of plus 3 or more, it means there is a solid bid below the market, and the buy-the-dip crowd is dominant.

VIX and Bollinger Bandwidth – our two indicators of market volatility – have settled down recently. Is this a sign that better days lie ahead? Or is it the calm before the storm? My money is on better days ahead, but not for very much longer.

Moving Averages are still positive, but getting less so. It’s too early to make a judgement about this indicator, except to say that we are now just 3% above the 200 day moving average for the S&P 500.

Chart readers will notice if we pierce that barrier, and newsletters will go out to subscribers, warning of worse things to come.

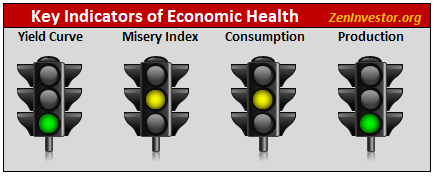

Key Recession Indicators (KRI)

This graphic, and the data that supports it, is intended to give readers a quick visual sense of economic health.

The risk of the US economy sliding into recession in the next 6 months is a moderate 26% as of the end of April. We base this estimate on a combination of factors (see the table below) that have proven accurate in calling turns in the business cycle. Our model will tell us when the conditions are in place for a move to a more defensive, or risk-off stance. Until that happens, it’s steady as she goes.

Yield Curve. The curve has been flattening for several months, without tipping over into an inversion. If this continues, this light will remain green.

Misery Index. This index helps determine how the average citizen is doing economically. It is calculated by adding the seasonally adjusted unemployment rate to the annual inflation rate. It is assumed that both a higher rate of unemployment and a worsening of inflation will create economic and social costs for all.

Consumption. This set of indicators measures the health of those who buy the goods and services that are produced, sold, and distributed. A health economy needs healthy consumers of these goods and services.

Production. This is the flip-side of the consumption indicators. For the economy to grow and create new jobs, businesses must be healthy enough to invest in new ideas, products and services that consumers need.

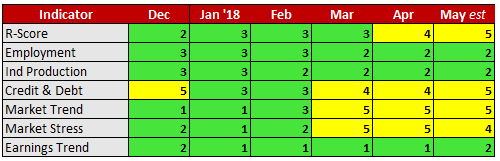

The Coincident Indicators

R-Score. This indicator combines the treasury yield curve, inflation, and unemployment.

Employment. YoY % Chg. in private non-farm employment.

Ind Production. YoY % Chg. in industrial production.

Credit & Debt. Difference between Junk bond yield and Treasury bond yield.

Market Trend. YoY % Chg. in the S&P 500 index.

Market Stress. Combination of stock market price change and the unemployment rate change.

Earnings Trend. YoY % Chg.; Beats; Revisions; Upgrades.

The latest estimates (for May 2018) show a slight deterioration from last month’s numbers. Three of our indicators, R-Score, Credit, and Earnings Trend, have slipped from where they were last month. But note that there are no red cells in this table. Until we begin to see red, it’s business as usual.

The takeaway from all of this is that the economy is strong enough to support the stock market. In the absence of a recession, corrections in the stock market are limited in scope and duration. It’s not unusual to see a 10% to 15% decline in the market without a recession taking place.

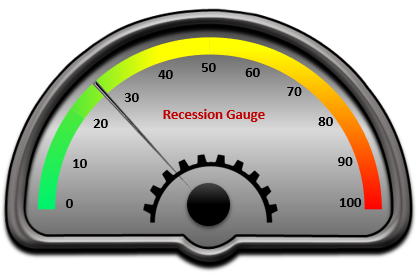

Recession Probability Gauge

This is a tool that my clients and subscribers can use to help them make critical asset allocation decisions. This is not a market-timing tool. It’s a dynamic reading of the probability that a new recession will arrive sometime in the next 12 months.

As of today, May 31, 2018, the probability of a recession beginning within the next 12 months is 26%. This is a significant increase over last month’s 14% reading. But there is no need to take any defensive action right now. I still believe that the market will make another new high before it finally rolls over.

Armed with this information, investors can decide for themselves how to use it. Highly risk-averse investors might cut back on equity exposure when the risk is 20% or higher. Less risk-averse investors may decide to wait until the probability reaches 30%, or 40%, or whatever threat level triggers them to play defense.

Probabilities of various outcomes over the next 6 months

Moderate expansion of 2.5-3% …….62%

Strong expansion of 3.5-4.5% GDP growth ……5%

Growth recession of 1-2% GDP growth ……7%

Outright recession with negative GDP growth ……26%

Final Thoughts

As I said at the start of this report, the stock market is in a funk. The longer this correction drags on, the more likely it will resolve itself negatively. However, it would be a mistake to jump the gun and start bailing out now. Some of the most profitable months I’ve experienced as an investor came after just this kind of market funk. I don’t want to eliminate the possibility of participating in another leg up, and so I advise readers to wait for now. If you already have a fully-formed Plan B, great. If you don’t, now is the time to work on it.

Your Plan B

When I work with investors in a coaching or consulting arrangement, one of the things we work on is contingency planning. It’s not as easy as you may think. To do it right, you must be willing to be radically honest about your behavioral tendencies and biases. If you know, for example, that you tend to hold on to losing positions long past their sell-by date, you must factor that into your contingency plan.

There are several other key behavioral traps and biases that are common for non-professionals, and we try to get them all out on the table, so we can set up a structure with price parameters and checklists, with the goal of taking as much emotion out of the process as possible.

I know that many of you are anxious about where the market might take us next, and so am I. That’s why I have evidence-based models to guide my decision-making.